The Passive Investing Paradox

For two decades, a simple message has dominated financial media: stop trying to beat the market and just buy an index fund.

The logic sounds irresistible. Most active managers underperform their benchmark over long periods, fees eat into returns, and the market is "efficient." But this narrative, while partially true, conceals a growing structural problem that passive investors ignore at their peril.

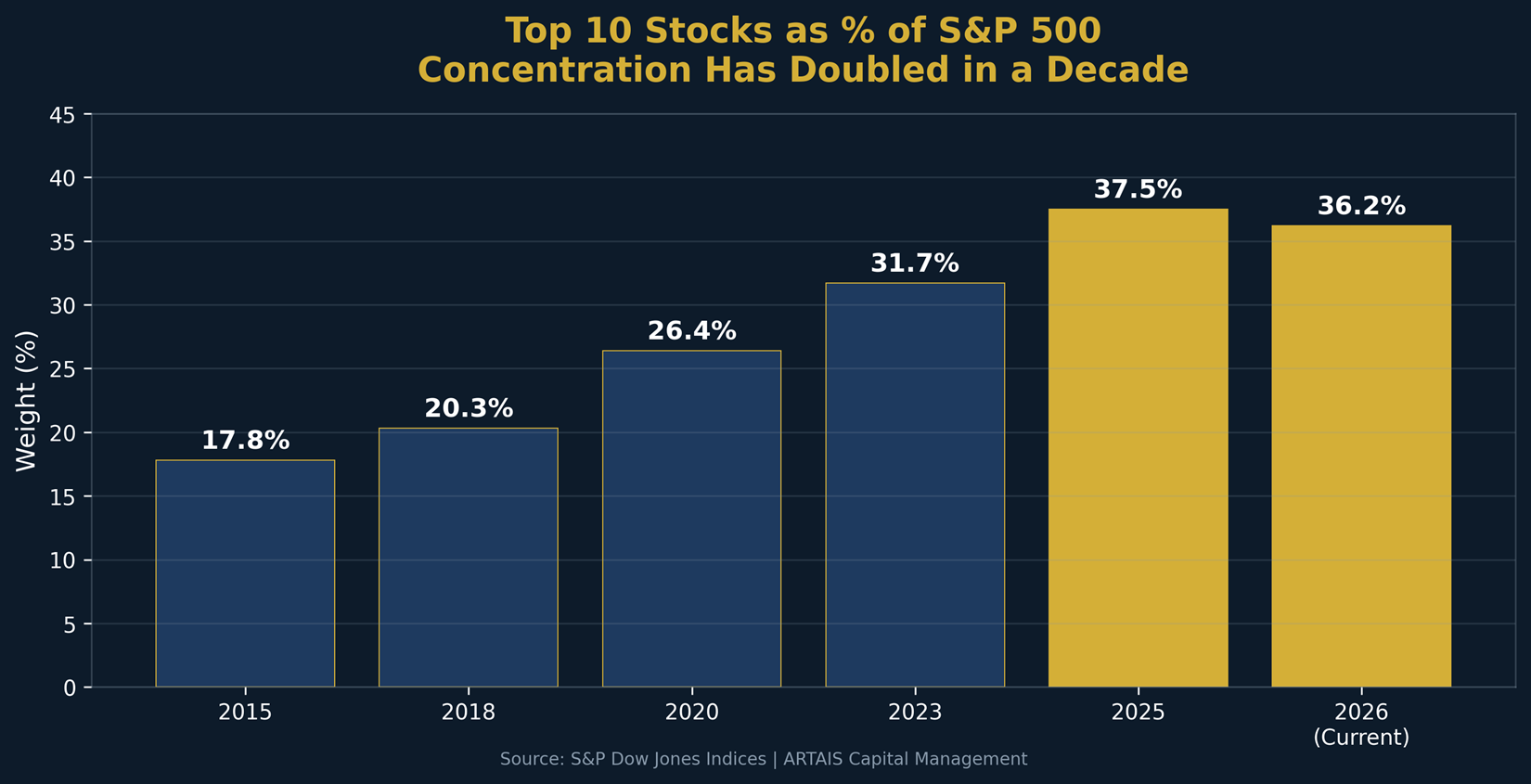

When you buy the S&P 500 today, you are not buying 500 stocks in equal measure. You are making a concentrated bet on a handful of mega-cap technology companies.

As of April 2026, the top 10 stocks in the S&P 500 account for approximately 35.6% of the entire index, according to S&P Dow Jones Indices. That figure sat around 18% just a decade ago.

Buying "the index" is no longer the diversified strategy it once was.

The Concentration Problem Is Real

This concentration creates a feedback loop. As more money flows into passive index funds, it disproportionately bids up the largest stocks, regardless of their fundamentals.

A dollar invested in an S&P 500 index fund sends roughly 7 cents to Nvidia alone.

The result is a market where the biggest companies get bigger simply because they are the biggest, not because their earnings growth justifies it.

The divergence between cap-weighted and equal-weighted S&P 500 performance tells the story. Over the past 10 years, the cap-weighted S&P 500 (SPY) returned 14.9% annualized, while the equal-weighted version (RSP) returned 11.6% annualized.

That 3.3 percentage point gap is almost entirely driven by the outsized performance of a handful of mega-cap names. If those names stumble, passive investors bear the full weight of the decline.

Where Active Managers Earn Their Keep

The SPIVA U.S. Scorecard for mid-year 2025 revealed an important shift: 75% of actively managed mid-cap funds and 78% of small-cap funds outperformed their benchmarks over the first half of 2025.

Even among large-cap managers, 46% outperformed in that same period, a meaningful improvement from the 35% rate seen in 2024.

Active management tends to add value in three specific environments:

- volatile and declining markets, where managers can raise cash or rotate defensively;

- concentrated markets, where a handful of stocks drive the index and active managers can avoid overvalued names;

- and inefficient market segments, such as small-caps, international, and credit markets, where information advantages still exist.

The real argument for active management is not that every active manager beats the index. It is that a disciplined, rules-based active approach can manage risk, adapt to changing market regimes, and avoid the blind concentration that passive investing now demands.

Not all active management is created equal. At ARTAIS Capital, we use a rules-based, adaptive approach designed to navigate changing market regimes, without the blind concentration that index investing now demands.

If you would like to learn more about our strategy and how to become a client, schedule a conversation.

Sources

1. S&P Dow Jones Indices — SPIVA U.S. Mid-Year 2025 Scorecard — spglobal.com

2. Yahoo Finance — SPY, RSP historical price data — finance.yahoo.com

3. S&P Dow Jones Indices — S&P 500 constituent weights — April 2026

4. AhaSignals — S&P 500 Concentration Risk Dashboard — ahasignals.com