Managing Risk Is The Foundation For Growth

Most investors focus on returns. What they should focus on is losses.

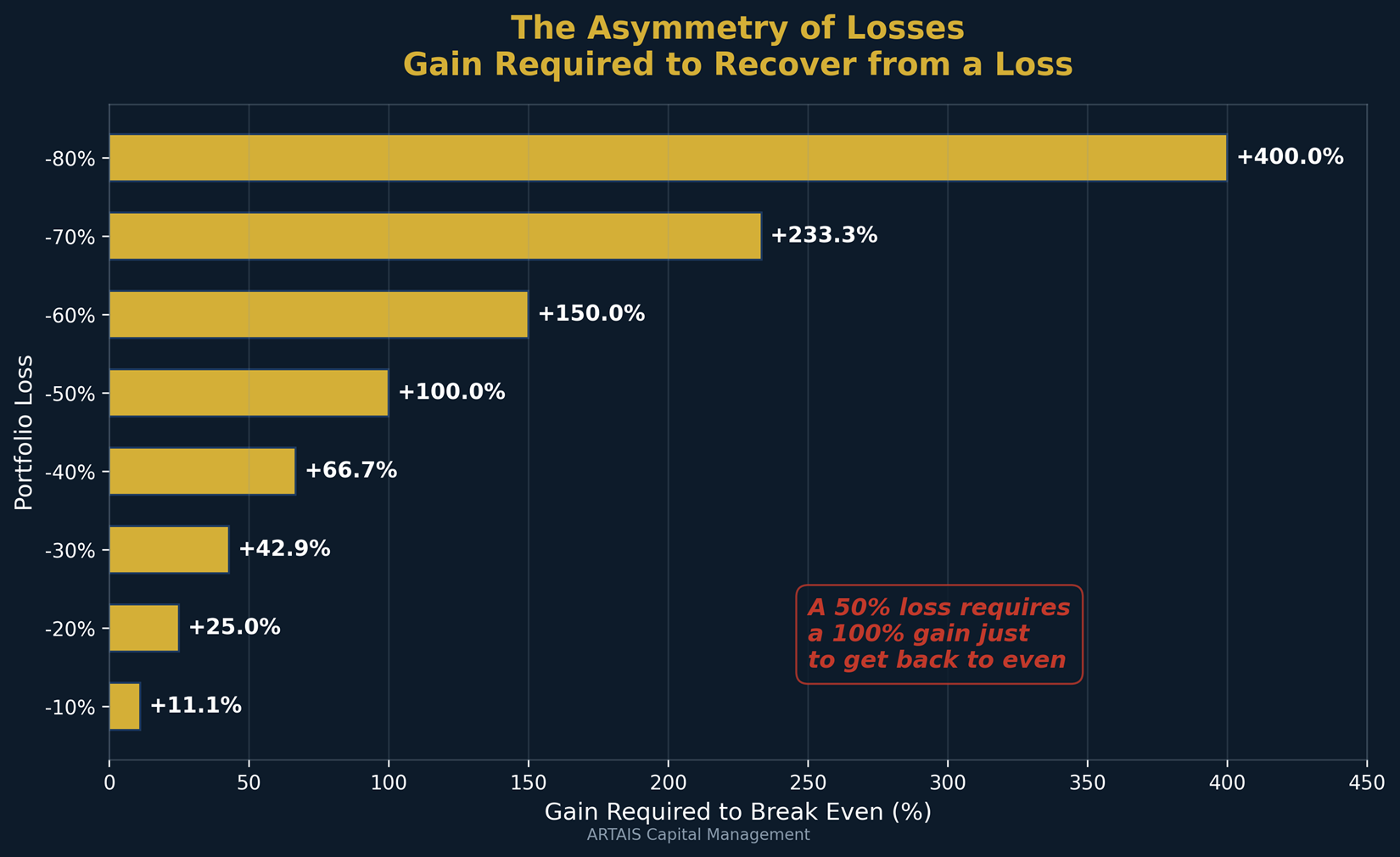

The mathematics of compounding are unforgiving: losses and gains are not symmetrical.

A portfolio that drops 50% needs a 100% gain just to get back to where it started. A 33% loss requires a 50% gain to recover.

These are not abstract numbers — they are the defining challenge of every investor who lived through the dot-com crash, the 2008 financial crisis, or the 2022 bear market.

This asymmetry explains why two portfolios with identical average returns can produce dramatically different outcomes.

A portfolio that returns +30%, -20%, +30%, -20% over four years has an average annual return of +5%. But the actual compounded return is only +2.0%.

The volatility itself destroys wealth — a phenomenon known as volatility drag or variance drain.

The smoother the path, the more money you keep.

The Historical Cost of Staying Fully Invested

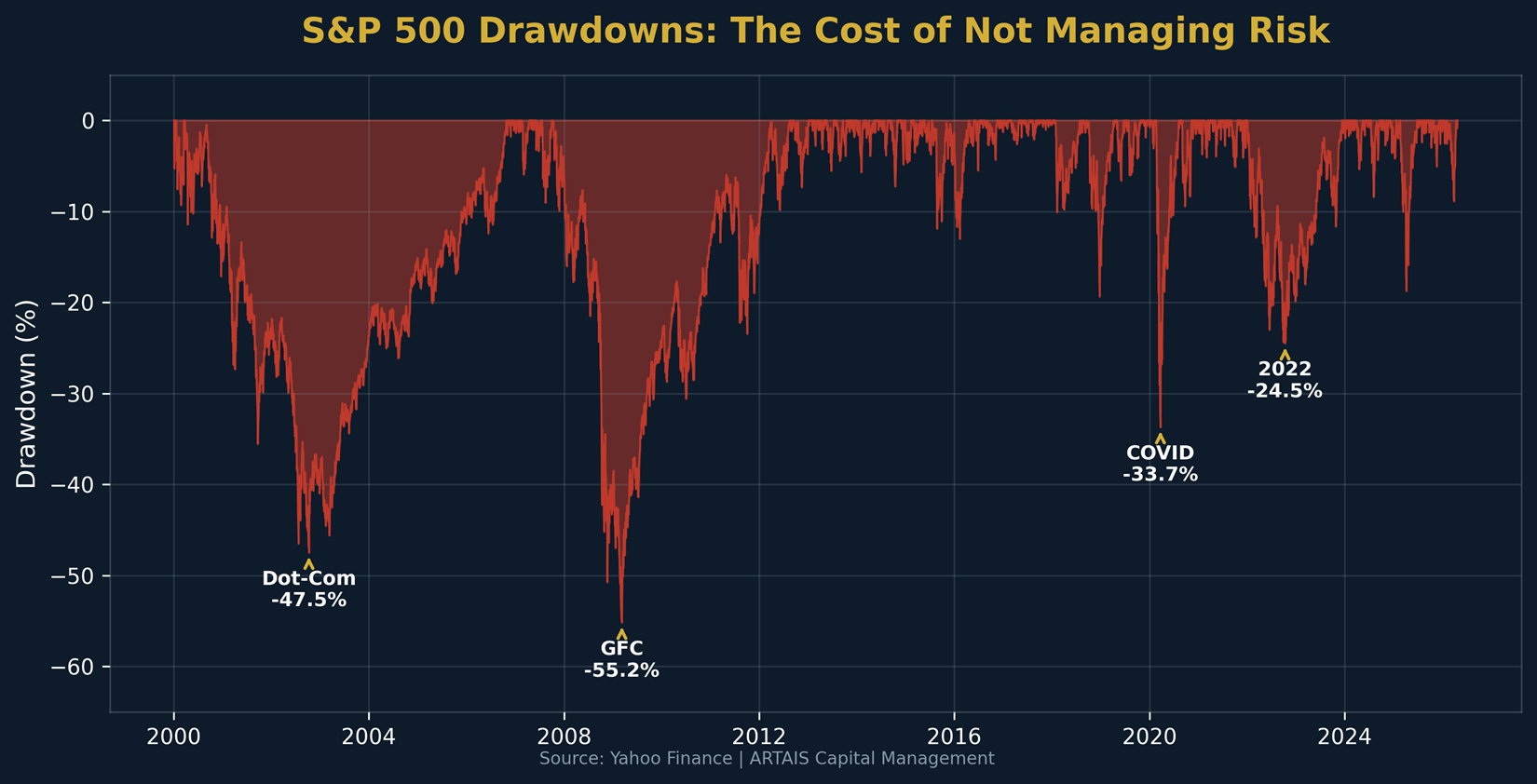

The S&P 500 has experienced four major drawdowns since 2000, each extracting a devastating toll on portfolios and, more importantly, on the investors holding them:

Dot-Com Crash (2000-2002): The S&P 500 fell 47.5% from peak to trough. It took 6.6 years to recover to the prior high. An investor who held $1 million at the peak watched it shrink to $525,000 — and did not see $1 million again until October 2006.

Global Financial Crisis (2007-2009): The S&P 500 fell 55.2%, its worst decline since the Great Depression. Recovery took 4.9 years. A $1 million portfolio dropped to $448,000.

COVID Crash (February-March 2020): A swift 33.7% decline over just 23 trading days, followed by an unusually rapid 5-month recovery.

2022 Bear Market: A 24.5% decline driven by aggressive Fed rate hikes and inflation, with recovery taking 1.9 years.

The Behavioral Trap

The real damage from large drawdowns is not just mathematical — it is behavioral.

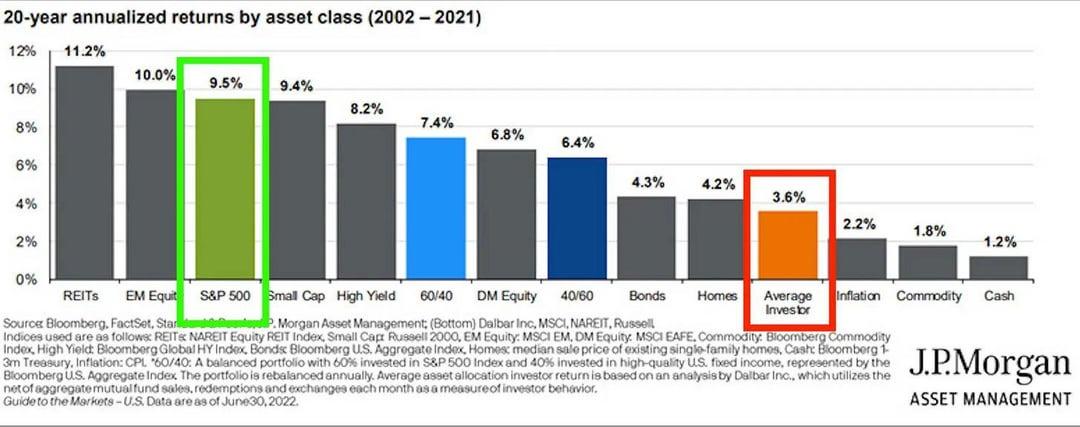

Historically, investors have not kept up with the market:

Why? Because investors panic-sell during drawdowns, lock in losses, and then re-enter the market after the recovery has already occurred.

A study done by DALBAR found one of the main reasons the average investor earns significantly less than the market is because they cannot endure the drawdowns that buy-and-hold demands.

This is the strongest argument for risk management.

If a strategy that captures 80% of the upside but avoids 60% of the downside keeps an investor fully invested and eliminates panic selling, the net result may far exceed what pure buy-and-hold delivers in practice — not in theory, but in practice, for real human beings with real emotions.

At ARTAIS Capital, risk managment ins't an afterthought, it's the foundation of our strategy. The goal of our systematic approach is to participate in rising markets while seeking to limit bear market drawdowns.

If you would like to learn more about our strategy, contact us here.

Sources

1. Yahoo Finance — SPY historical adjusted close prices — finance.yahoo.com

2. DALBAR — 2025 QAIB Report (2024 data) — dalbar.com — March 2025

3. DALBAR — 2026 QAIB Report (2025 data) — dalbar.com — April 2026

- JP Morgan